At a time when fixed income and low-risk investments are gaining traction, the Post Office Monthly Income Scheme (MIS) has once again emerged as one of the most reliable options for Indian savers. Backed by the Government of India, the scheme continues to attract investors in 2026 with its promise of stable monthly earnings and capital safety.

What is Post Office MIS?

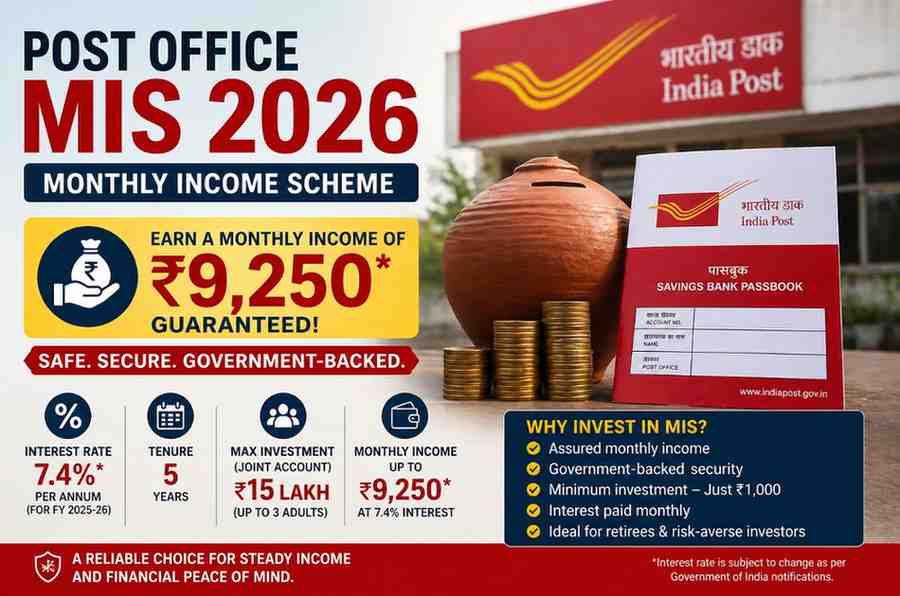

The Post Office Monthly Income Scheme (POMIS) is a small savings scheme offered by India Post that provides guaranteed monthly income on a lump sum investment.

Unlike fixed deposits where interest is often paid quarterly or at maturity, MIS ensures monthly payouts, making it especially popular among retirees and conservative investors.

- Government-backed (low risk)

- Fixed returns for the entire tenure

- Monthly income credited directly

Interest rate in 2026

For FY 2025–26, the interest rate on MIS remains:

- 7.4% per annum (paid monthly)

The rate is set by the government and reviewed quarterly, but once you invest, your interest rate remains locked for 5 years.

How you can earn ₹9,250 per month

The headline figure of ₹9,250 monthly income comes from maximum investment in a joint account.

Here’s how it works:

- Maximum investment (single account): ₹9 lakh

- Maximum investment (joint account): ₹15 lakh

At 7.4% interest:

- ₹9 lakh → ~₹5,550/month

This makes MIS one of the few government schemes offering predictable monthly cash flow.

Key features of the scheme

1. Fixed tenure

The scheme has a 5-year lock-in period, after which you can withdraw or reinvest.

2. Minimum investment

You can start with as little as ₹1,000, making it accessible to a wide range of investors.

3. Monthly income payout

Interest is calculated annually but paid every month, ensuring steady income.

4. Joint account advantage

Up to three adults can open a joint account, increasing the investment limit and income potential.

5. Capital safety

Being a government-backed scheme, it is considered one of the safest investment options in India.

Who should invest?

The MIS scheme is particularly suitable for:

- Retirees looking for steady income

- Salaried individuals seeking passive income

- Risk-averse investors

- Families wanting predictable monthly cash flow

It is not ideal for those seeking high growth or market-linked returns.

Tax rules you should know

- Interest earned is fully taxable as per your income slab

- No tax deduction under Section 80C

- No TDS is deducted, but tax liability remains

Premature withdrawal rules

While MIS is a 5-year scheme, early exit is allowed with penalties:

- Before 3 years: 2% deduction

- After 3 years: 1% deduction

This ensures some flexibility, though it is designed as a medium-term investment.

How it compares to other schemes

Compared to other post office savings options:

- Higher than savings account returns

- Lower than Senior Citizen Savings Scheme (but with monthly payout)

- More stable than market-linked investments

MIS stands out primarily for its monthly income feature, which most other schemes do not offer.

The bottom line

The Post Office Monthly Income Scheme (POMIS) remains a “superhit” option in 2026 for investors who prioritise safety, stability, and regular income over high returns.

With the ability to generate up to ₹9,250 per month from a joint investment, it continues to serve as a dependable financial tool especially in uncertain market conditions.

For those looking to build a predictable income stream without taking risks, MIS remains one of the strongest government-backed options available today.

Input & Images : Hindusthan Samachar

Add outlooknews.in as preferred source on google – click here

Also read –

Cheapest turbo petrol SUVs in India: Powerful performance, fun driving at prices starting under ₹9 lakh — all you need to know

Last Updated on: Thursday, April 30, 2026 5:00 pm by Monisha Angara | Published by: Monisha Angara on Thursday, April 30, 2026 5:00 pm | News Categories: Business