India’s micro, small and medium enterprises (MSMEs) continue to sit at the heart of the country’s economic engine, contributing significantly to employment, exports and grassroots entrepreneurship. As India moves deeper into 2026, the government’s policy focus on strengthening MSMEs has sharpened, particularly around easing access to affordable, collateral-free credit.

For small entrepreneurs, startups in manufacturing and services, and first-time business owners, the biggest hurdle often remains financing. Traditional bank loans still demand collateral, detailed credit histories and long approval timelines. To address this, the Union government has expanded and refined several flagship schemes that aim to reduce risk for lenders while empowering entrepreneurs.

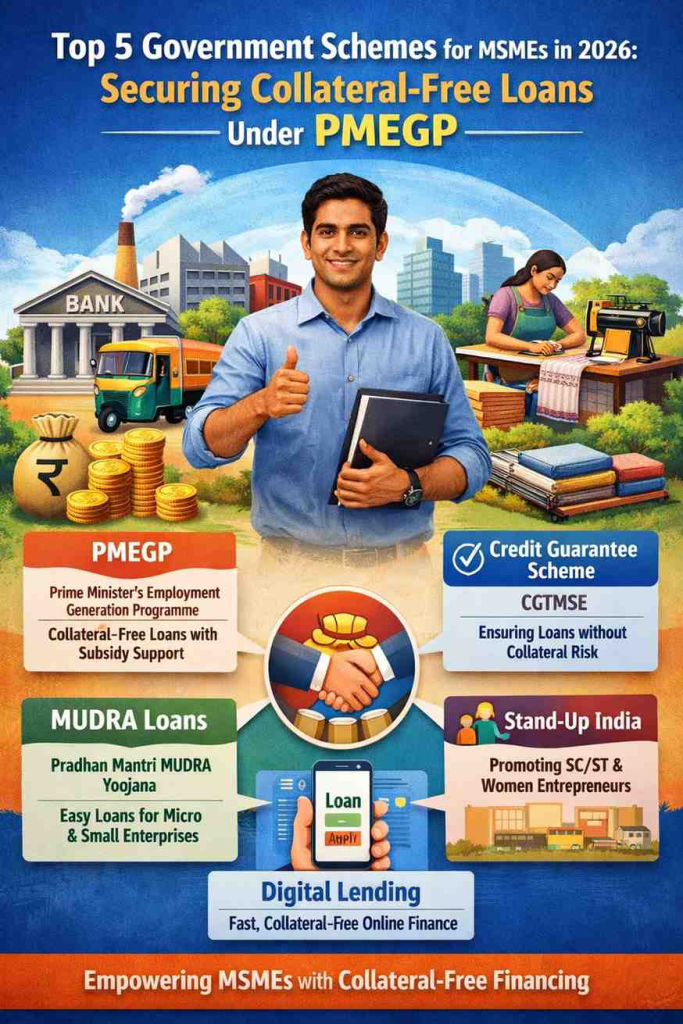

Among these, the Prime Minister’s Employment Generation Programme (PMEGP) remains one of the most relevant pathways for collateral-free loans. However, it is most effective when understood alongside other complementary MSME schemes. Here is an in-depth look at the top five government schemes MSMEs should know in 2026—and how PMEGP fits into the larger credit ecosystem.

PMEGP: The Backbone of Collateral-Free Financing for New Entrepreneurs

The Prime Minister’s Employment Generation Programme continues to be a cornerstone scheme for first-time entrepreneurs and micro enterprises in both rural and urban India. Implemented by the Khadi and Village Industries Commission (KVIC), PMEGP is designed to encourage self-employment by providing bank credit linked with government subsidy.

Under PMEGP, eligible beneficiaries can secure loans without providing collateral for projects up to the prescribed limit, as these loans are covered under the Credit Guarantee Fund. In 2026, the scheme remains especially attractive for small manufacturing units, service enterprises and traditional artisans looking to modernise or scale operations.

What makes PMEGP stand out is the margin money subsidy, which reduces the effective loan burden on the entrepreneur. Depending on the category and location, the subsidy can range significantly, lowering the repayment pressure during the initial years of operation. For many micro entrepreneurs, this support bridges the critical gap between an idea and a viable business.

Credit Guarantee Scheme for MSMEs: The Safety Net Behind Collateral-Free Loans

While PMEGP helps initiate enterprises, the Credit Guarantee Scheme for Micro and Small Enterprises (CGTMSE) plays a silent but crucial role in expanding access to finance. This scheme provides a government-backed guarantee to banks and financial institutions, encouraging them to extend loans without collateral.

In 2026, CGTMSE coverage has become more streamlined, with improved digital processing and faster claim settlements. This has increased lender confidence, making it easier for MSMEs to secure working capital and term loans even beyond the startup phase.

For entrepreneurs applying under PMEGP, CGTMSE often acts as the underlying risk cushion for banks, ensuring that collateral requirements are waived. Understanding this linkage helps MSMEs better negotiate with lenders and structure their financing needs.

MUDRA Loans: Fuel for Micro and Small Enterprises at Every Stage

The Pradhan Mantri MUDRA Yojana (PMMY) remains one of the most widely used credit schemes for micro enterprises. By 2026, MUDRA loans have evolved to cater not just to very small businesses but also to growth-oriented enterprises transitioning from informal to formal operations.

MUDRA loans are divided into stages based on business maturity, offering flexibility in loan amounts and repayment structures. Like PMEGP, these loans are collateral-free and accessible through banks, NBFCs and microfinance institutions.

For entrepreneurs who may not qualify for PMEGP due to sectoral or eligibility constraints, MUDRA serves as a parallel pathway to access credit. Many MSMEs also use MUDRA loans as follow-on funding after exhausting PMEGP benefits.

Stand-Up India: Targeted Support for Inclusive Entrepreneurship

Stand-Up India continues to focus on promoting entrepreneurship among women and individuals from Scheduled Castes and Scheduled Tribes. In 2026, the scheme has gained renewed importance as part of the government’s broader push for inclusive growth.

The scheme facilitates bank loans for greenfield enterprises in manufacturing, services and trading sectors, with structured handholding support. While not exclusively collateral-free in all cases, Stand-Up India loans are often backed by credit guarantee mechanisms that reduce the need for traditional security.

For eligible entrepreneurs, Stand-Up India can complement PMEGP by providing higher loan amounts and longer tenures, particularly for enterprises with expansion plans.

MSME Digital Lending and Emergency Credit Support Frameworks

Building on lessons from previous economic disruptions, the government has continued to strengthen digital and emergency credit frameworks for MSMEs. In 2026, these initiatives focus on faster disbursals, data-driven credit assessment and minimal documentation.

Digital platforms now integrate GST data, bank statements and credit histories to offer pre-approved or quick-turnaround loans, many of which remain collateral-free under guarantee schemes. For PMEGP beneficiaries, these platforms provide easier access to additional working capital once the enterprise becomes operational.

These digital credit pathways signal a shift in MSME financing—from relationship-based lending to ecosystem-based support—where government schemes, fintech platforms and banks work together.

How MSMEs Can Strategically Use PMEGP in 2026

For entrepreneurs in 2026, PMEGP works best when approached as part of a long-term financing strategy rather than a one-time subsidy. Proper project planning, realistic revenue projections and clear understanding of subsidy norms are critical to securing approval.

Applicants who align PMEGP funding with credit guarantee schemes and digital lending options stand a better chance of sustaining and scaling their businesses. Banks, too, are increasingly looking for enterprises that demonstrate awareness of multiple schemes and responsible credit planning.

The Bigger Picture for MSMEs

As India targets higher manufacturing output, exports and job creation, MSMEs will remain central to achieving these goals. The government’s focus in 2026 is not just on launching new schemes, but on improving execution, credit flow and accountability.

For small business owners, awareness is the first step. Understanding how PMEGP and other MSME schemes interact can unlock collateral-free credit that was once out of reach. In an environment where access to finance often determines survival, these schemes are not just policy instruments—they are lifelines for millions of entrepreneurs shaping India’s economic future.

Add outlooknews.in as a preferred source on google – click here

Last Updated on: Tuesday, January 27, 2026 10:46 am by Outlook News Team | Published by: Outlook News Team on Tuesday, January 27, 2026 10:46 am | News Categories: News