RBI Tightens Digital Lending Framework to Protect Borrowers and Strengthen Compliance

The Reserve Bank of India (RBI) has issued updated guidelines on digital lending, reinforcing its regulatory framework for banks and non-banking financial companies (NBFCs) operating through digital platforms and lending apps.

The move is significant for millions of Indian borrowers who use mobile apps for instant loans. It is also crucial for fintech companies and regulated entities that offer digital credit products.

The updated framework builds on earlier directions issued in September 2022, when the RBI first introduced detailed norms after concerns over unethical recovery practices, data misuse, and lack of transparency in digital lending.

The central bank’s latest clarification aims to improve transparency, borrower protection, and regulatory oversight in India’s fast-growing digital lending market.

Why the RBI’s Digital Lending Guidelines Matter

Digital lending in India has grown rapidly in recent years. Easy access to smartphones and UPI-based payments has increased demand for quick, small-ticket loans.

However, the sector also saw:

- Complaints about hidden charges

- Harassment by recovery agents

- Misuse of borrower data

- Unauthorized lending apps

To address these risks, the RBI introduced a structured regulatory approach. The updated guidelines further clarify compliance requirements and responsibilities of regulated entities.

The goal is simple: protect borrowers while supporting responsible innovation.

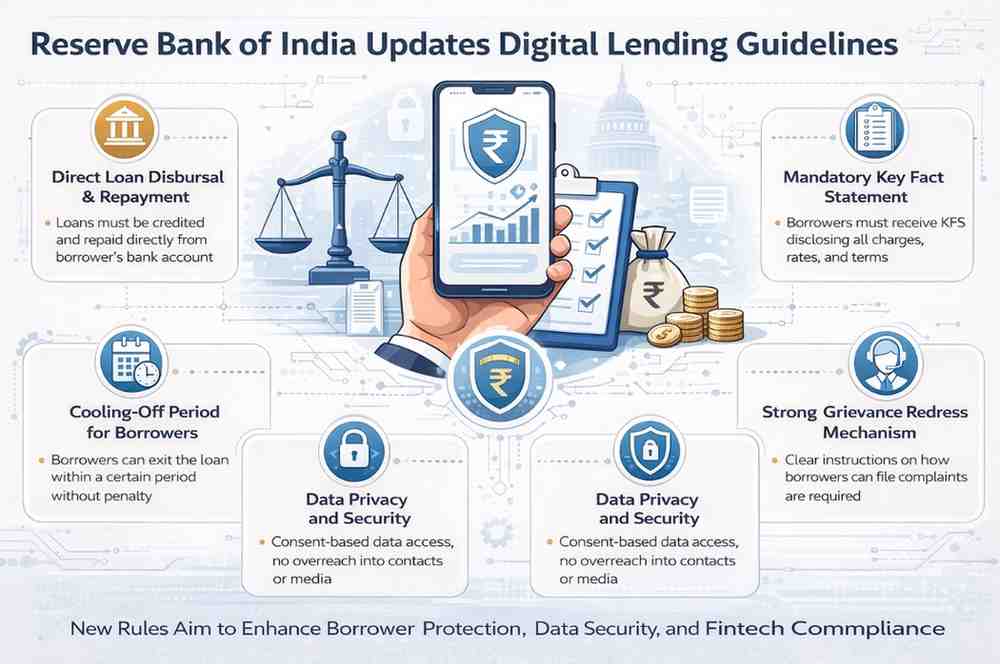

Direct Loan Disbursal and Repayment Rules

One of the key features of the RBI’s framework is the rule on loan disbursal and repayment.

Under the guidelines:

- Loan amounts must be directly credited to the borrower’s bank account.

- Repayments must also be made directly to the regulated entity’s bank account.

This means third-party pool accounts or pass-through accounts are not allowed, except in specific, permitted cases.

This rule increases transparency and ensures that borrowers know exactly who is providing the loan.

Mandatory Key Fact Statement (KFS)

The RBI has made it mandatory for lenders to provide a Key Fact Statement (KFS) to borrowers before executing a digital loan agreement.

The KFS must clearly mention:

- Loan amount

- Interest rate

- Annual Percentage Rate (APR)

- Processing fees

- Penal charges

- Loan tenure

No hidden charges can be imposed if they are not mentioned in the KFS.

This requirement improves transparency and helps borrowers compare loan offers more easily.

Cooling-Off Period for Borrowers

To protect consumers, the RBI introduced a cooling-off or look-up period.

During this period:

- Borrowers can exit the digital loan by paying the principal and proportionate charges.

- No penalty can be imposed for early exit within the cooling-off window.

The exact duration of the cooling-off period is decided by the regulated entity’s board but must be clearly disclosed to borrowers.

This measure prevents borrowers from being trapped in high-cost loans without understanding the terms.

Data Privacy and Consent-Based Access

Data privacy has been one of the biggest concerns in digital lending.

The RBI has made it clear that:

- Lending apps can only collect data that is necessary for loan processing.

- Explicit borrower consent is required before accessing personal data.

- Access to mobile phone data such as contacts or media files is not permitted unless strictly necessary and legally compliant.

Borrowers must also have the option to withdraw consent.

This aligns digital lending practices with broader data protection principles.

Regulated Entities Remain Fully Responsible

Even when banks or NBFCs partner with fintech companies or lending service providers (LSPs), the responsibility lies with the regulated entity.

In simple terms:

- Banks and NBFCs cannot shift regulatory responsibility to third-party apps.

- They must ensure that digital lending partners follow RBI rules.

This ensures accountability and reduces the risk of unregulated lending activities.

Grievance Redress Mechanism Must Be Clearly Displayed

The RBI guidelines require that all digital lending platforms clearly display:

- The name of the regulated entity

- Customer care contact details

- Grievance redress mechanism

- Details of the RBI’s complaint portal

Borrowers should know where to complain in case of unfair practices.

This step strengthens consumer confidence in digital lending platforms.

Impact on Fintech Companies and NBFCs

The updated guidelines have important implications for India’s fintech ecosystem.

Companies offering digital loans must:

- Review their business models

- Ensure full compliance with RBI rules

- Update loan agreements and disclosures

- Strengthen data protection systems

While compliance costs may increase, the framework provides long-term stability and credibility to the sector.

Industry experts believe that clear regulation can help serious players grow while filtering out non-compliant operators.

Background: RBI’s 2022 Digital Lending Directions

In September 2022, the RBI issued comprehensive Digital Lending Guidelines after reviewing recommendations of a working group on digital lending.

The key objectives were:

- Prevent unfair lending practices

- Improve transparency

- Protect borrower data

- Ensure regulatory oversight

The updated guidance reinforces those objectives and provides further clarity to regulated entities.

What Borrowers Should Check Before Taking a Digital Loan

With the updated RBI framework in place, borrowers should still exercise caution.

Before accepting a digital loan offer, check:

- Is the lender a bank or RBI-registered NBFC?

- Have you received a Key Fact Statement?

- Are all charges clearly disclosed?

- Is there a cooling-off option?

- Is customer support information clearly mentioned?

Borrowers can verify registered NBFCs through the RBI’s official website.

Awareness remains the strongest protection.

Digital Lending in India: Growth and Challenges

India’s digital credit market has expanded due to:

- UPI adoption

- Smartphone penetration

- E-commerce growth

- Demand for short-term credit

However, the sector also faced scrutiny due to reports of illegal lending apps and unethical recovery methods.

The RBI’s regulatory action aims to balance innovation with consumer protection.

Responsible digital lending can help expand financial inclusion, especially for individuals and small businesses with limited access to traditional credit.

RBI’s Focus on Financial Stability and Consumer Safety

The RBI’s approach reflects its broader mandate to maintain financial stability.

By tightening norms on digital lending, the central bank is:

- Reducing systemic risks

- Improving transparency

- Strengthening trust in digital finance

As digital credit becomes more common, clear regulation is essential to prevent misuse and protect vulnerable borrowers.

Looking Ahead: What to Expect Next

Going forward, digital lending platforms may see:

- Stronger compliance checks

- Increased supervision

- Standardized disclosure formats

- Enhanced consumer awareness

The RBI may also continue to review the sector as technology evolves.

For borrowers, the updated framework offers greater protection. For lenders, it sets clear rules of operation.

Conclusion

The updated digital lending guidelines from the Reserve Bank of India mark an important step in strengthening India’s digital finance ecosystem.

By enforcing direct disbursal rules, mandatory Key Fact Statements, data privacy protections, and grievance redress mechanisms, the RBI has reinforced consumer safeguards.

As digital lending continues to grow in India, responsible practices and strict compliance will be critical.

For borrowers and fintech companies alike, the message is clear: transparency, accountability, and data protection are no longer optional – they are mandatory under RBI regulations.

Disclaimer: The information presented in this article is intended for general informational purposes only. While every effort is made to ensure accuracy, completeness, and timeliness, data such as prices, market figures, government notifications, weather updates, holiday announcements, and public advisories are subject to change and may vary based on location and official revisions. Readers are strongly encouraged to verify details from relevant official sources before making financial, investment, career, travel, or personal decisions. This publication does not provide financial, investment, legal, or professional advice and shall not be held liable for any losses, damages, or actions taken in reliance on the information provided.

Last Updated on: Monday, February 16, 2026 3:35 pm by Outlook News Team | Published by: Outlook News Team on Monday, February 16, 2026 3:35 pm | News Categories: Business