The Union Budget is not just a statement of government accounts; for millions of Indian households, it quietly shapes everyday decisions — from grocery bills and fuel costs to savings plans and long-term financial security. The Union Budget 2026–27 arrives at a time when families are closely watching inflation, interest rates, job stability and the rising cost of living. While macroeconomic targets dominate headlines, the real story lies in how budgetary decisions trickle down into monthly household expenses and savings behaviour.

This year’s budget places strong emphasis on balancing growth with fiscal discipline, and its impact will be felt across income groups in subtle but significant ways.

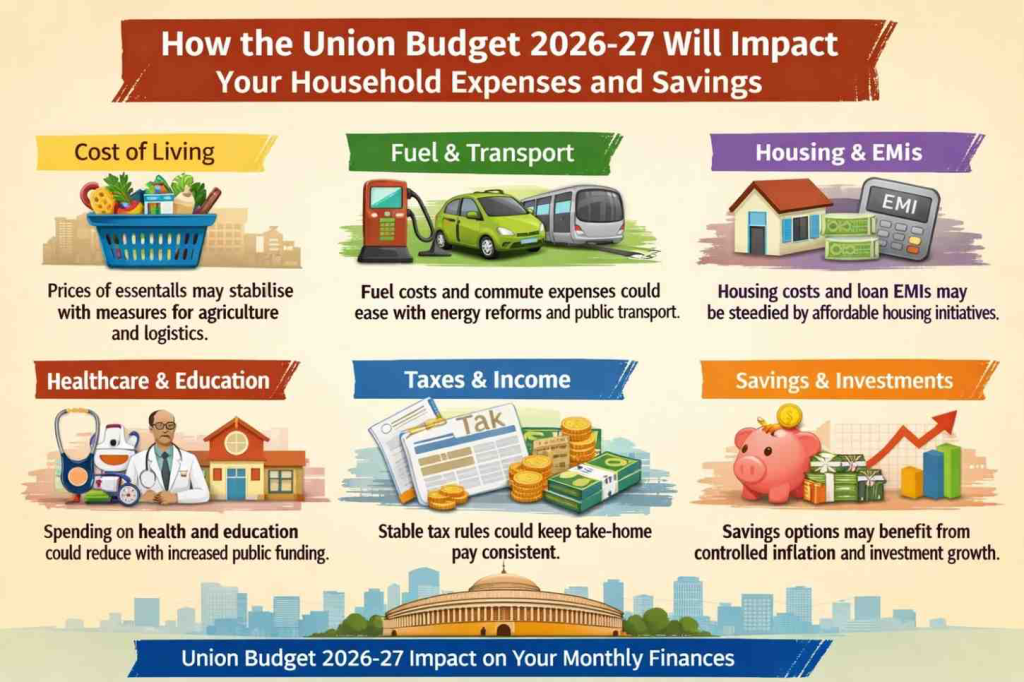

Cost of Living and Daily Essentials: What Changes at Home

One of the first areas households notice after a budget is the price of everyday essentials. While the government avoids dramatic tax shocks on basic consumption items, policy signals in the budget influence prices through supply chains and logistics costs.

Increased allocations for agriculture, food storage, and rural infrastructure are expected to stabilise prices of staples such as cereals, pulses, vegetables and edible oils over the medium term. For urban households, this may not translate into immediate price cuts, but it can help prevent sharp spikes during seasonal shortages.

At the same time, continued focus on transport infrastructure and freight efficiency is likely to reduce logistics costs gradually. When transportation becomes cheaper and faster, retailers pass on some benefits to consumers, helping keep grocery inflation under control. For families managing tight monthly budgets, even marginal relief in food inflation can make a noticeable difference.

Fuel, Electricity and Transport Expenses

Fuel prices have a cascading effect on household expenses, influencing everything from commuting costs to the price of essential goods. While the Union Budget 2026–27 refrains from major changes in fuel taxation, its push toward renewable energy and electric mobility has long-term implications.

Higher investments in solar power, battery storage and electric vehicle infrastructure aim to reduce dependence on imported fossil fuels. Over time, this could stabilise electricity tariffs and offer savings to households that adopt rooftop solar systems or electric two-wheelers. For middle-class families, lower electricity bills and reduced fuel expenses can free up money for savings or education-related spending.

Public transport investments announced in the budget are also expected to ease daily commuting costs in major cities. Expansion of metro networks, suburban rail and electric bus fleets can provide affordable alternatives to private vehicles, particularly for salaried employees and students.

Housing, Rent and Home Loan EMIs

Housing remains one of the biggest monthly expenses for Indian households, whether in the form of rent or home loan repayments. Budget 2026–27 continues its focus on affordable housing and urban development, which could ease pressure in the rental market over time.

Enhanced incentives for housing construction and urban infrastructure development are likely to increase housing supply in expanding cities. When supply improves, rental inflation tends to soften, benefiting young professionals and migrant workers. For homeowners, stable interest rates and continued support for housing finance institutions can prevent sudden spikes in EMIs.

Tax provisions linked to home loans and housing investments, even if unchanged, provide predictability. Households planning long-term purchases prefer stability, and the budget’s measured approach supports financial planning without sudden policy surprises.

Healthcare and Education Spending: Hidden Household Relief

Healthcare and education costs often rise silently, eating into household savings without immediate notice. Increased government spending in these sectors can indirectly reduce the financial burden on families.

With higher allocations for public healthcare infrastructure, diagnostic services and insurance coverage, households may face fewer out-of-pocket expenses during medical emergencies. For lower- and middle-income families, this acts as an invisible safety net, protecting savings that would otherwise be drained by hospital bills.

Similarly, investments in government schools, digital education platforms and skill development programmes can reduce dependence on expensive private alternatives. While private education will continue to grow, improved public systems offer families more choices and financial flexibility.

Taxes, Take-Home Income and Disposable Cash

The most closely watched aspect of any budget is personal taxation. While Budget 2026–27 focuses on widening the tax base rather than increasing tax rates, even small tweaks in exemptions and compliance rules can influence take-home income.

Stable income tax slabs and simplified compliance encourage households to plan expenses with confidence. For salaried individuals, predictable taxation helps in managing EMIs, insurance premiums and monthly savings commitments. Self-employed professionals and small business owners also benefit from clearer tax rules that reduce uncertainty and compliance costs.

When disposable income remains stable, households are more likely to maintain disciplined saving habits rather than dipping into emergency funds to meet routine expenses.

Savings, Investments and Financial Security

Beyond expenses, the budget shapes how households save and invest. Continued support for small savings schemes, pension systems and insurance penetration reinforces the importance of long-term financial security.

Interest rate signals and fiscal discipline in Budget 2026–27 aim to keep inflation in check, which is crucial for protecting the real value of savings. When inflation is controlled, fixed deposits, provident funds and pension contributions retain their purchasing power, benefiting conservative savers.

At the same time, policy encouragement for capital markets and digital finance platforms makes investing more accessible. For young earners, this creates opportunities to diversify savings beyond traditional instruments, potentially improving long-term wealth creation.

The Overall Household Balance Sheet

Taken together, the Union Budget 2026–27 may not dramatically change household expenses overnight, but it influences the broader environment in which families make financial decisions. Controlled inflation, steady taxation, improved public services and infrastructure-led growth all contribute to financial stability at the household level.

For most families, the real impact of the budget will be felt gradually — through fewer price shocks, steadier monthly expenses and better opportunities to save consistently. In an era of economic uncertainty, this quiet stability may be the most valuable takeaway from the Union Budget 2026–27.

Add outlooknews.in as a preferred source on google – click here

Last Updated on: Tuesday, February 3, 2026 10:43 am by Outlook News Team | Published by: Outlook News Team on Tuesday, February 3, 2026 10:43 am | News Categories: News