The Reserve Bank of India’s updated co-lending guidelines mark an important shift in how banks, non-banking financial companies (NBFCs), and fintech platforms collaborate to extend credit. As digital lending models mature and regulatory scrutiny intensifies, the new framework aims to balance innovation with consumer protection and financial stability. For fintech startups and NBFC partners, these changes redefine roles, responsibilities, and growth opportunities in India’s evolving credit ecosystem.

Why RBI Updated the Co-Lending Framework

Co-lending emerged as a way to improve credit access by combining the balance sheet strength of banks with the reach and agility of NBFCs and fintech platforms. However, rapid growth in digital lending also raised concerns around risk-sharing, transparency, customer protection, and regulatory accountability.

The RBI’s revised guidelines are designed to bring greater clarity and uniformity to co-lending arrangements. By tightening governance standards and clearly defining responsibilities, the regulator aims to ensure that credit expansion does not come at the cost of systemic risk or borrower exploitation.

Key Objectives Behind the New Guidelines

At the heart of the updated framework is the RBI’s focus on responsible lending. The guidelines seek to ensure that borrowers clearly understand who is lending to them, how interest rates are determined, and how grievances can be addressed. At the same time, the RBI wants lending institutions to maintain stronger oversight over credit underwriting and loan servicing.

Another key objective is to prevent regulatory arbitrage, where fintech-led models operate in grey areas between banks and NBFCs. By reinforcing accountability, the RBI aims to align co-lending practices with broader financial sector regulations.

What Has Changed in the Co-Lending Model

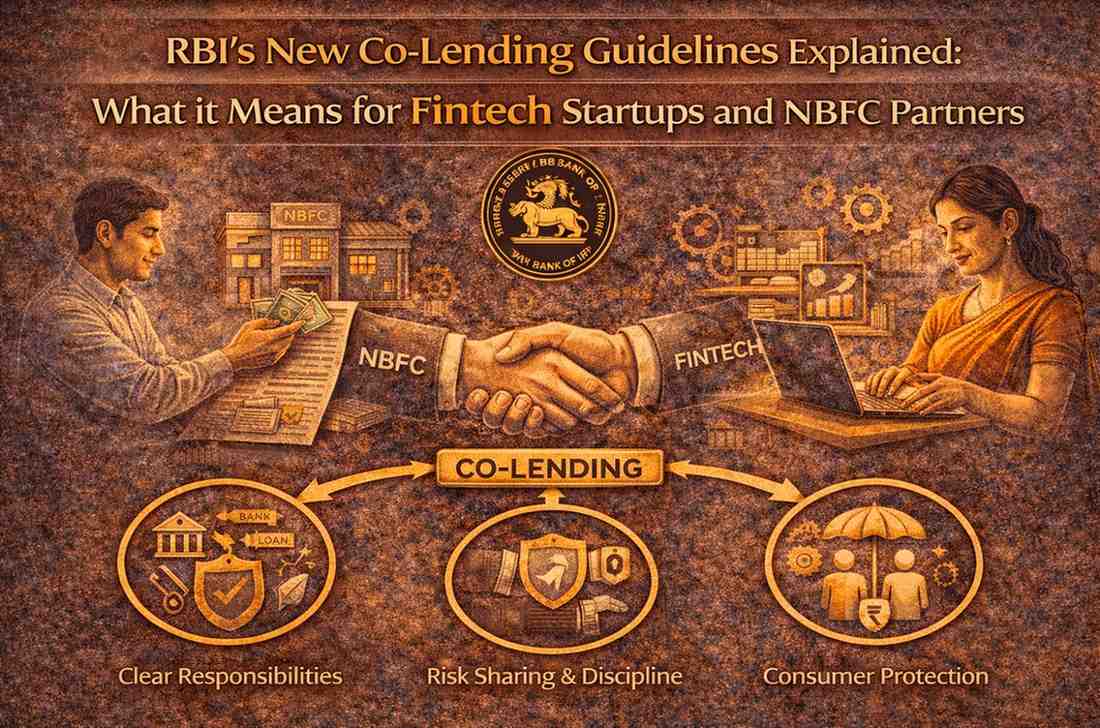

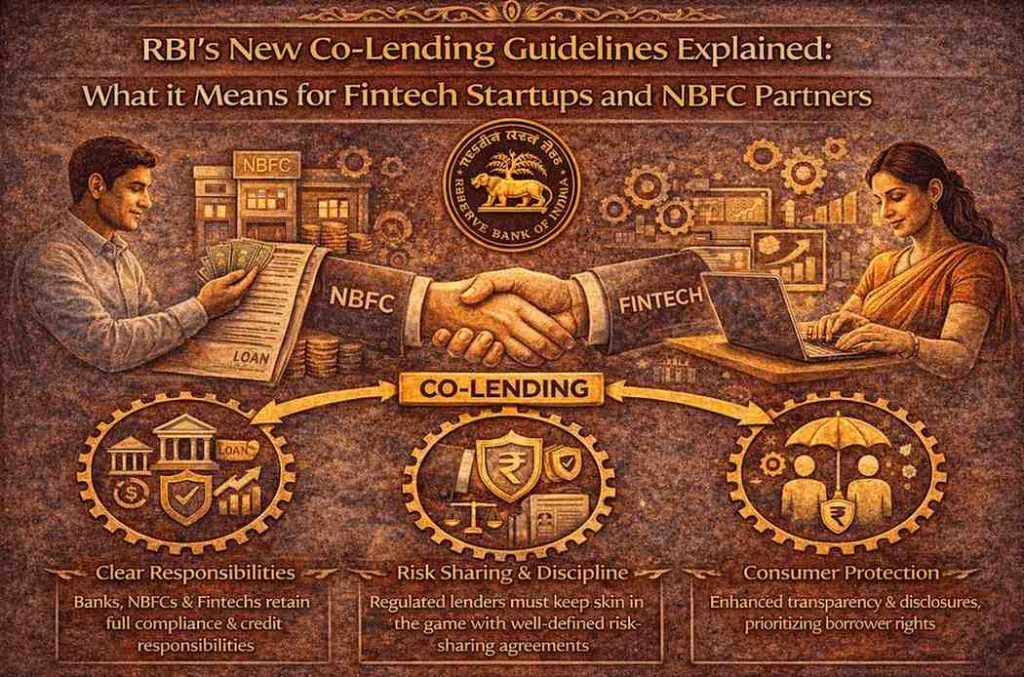

Under the revised guidelines, the regulated entities involved in co-lending—primarily banks and NBFCs—retain full responsibility for compliance, credit decisions, and customer protection. Fintech platforms, while still playing a key role in origination and technology support, cannot position themselves as lenders unless they are regulated entities.

The framework emphasises that all loans must be carried on the balance sheets of regulated lenders, with risk-sharing arrangements clearly documented. This reduces ambiguity around ownership of loans and ensures that accountability rests with entities under RBI supervision.

Implications for Fintech Startups

For fintech startups, the new guidelines bring both constraints and clarity. Startups that operate as lending service providers rather than licensed lenders will need to align closely with their bank or NBFC partners. Their role will increasingly focus on technology, customer acquisition, data analytics, and servicing support rather than credit decision-making.

While this may limit the degree of autonomy some fintechs previously enjoyed, it also offers greater legitimacy and stability. Clear regulatory boundaries can improve investor confidence and reduce the risk of sudden policy disruptions.

Impact on NBFC Partners

NBFCs remain central to the co-lending ecosystem under the revised guidelines. Their expertise in credit assessment, niche lending segments, and customer understanding continues to be valued. However, the new framework places greater compliance and governance responsibilities on NBFCs involved in co-lending arrangements.

NBFCs must ensure robust due diligence of fintech partners, transparent loan documentation, and effective grievance redressal mechanisms. While this increases operational complexity, it also strengthens the credibility of NBFC-led lending models.

Risk Sharing and Credit Discipline

One of the most significant aspects of the updated guidelines is the emphasis on clearly defined risk-sharing arrangements. The RBI expects participating lenders to retain meaningful exposure to the loans they originate, discouraging lax underwriting practices.

This approach aligns incentives between banks, NBFCs, and fintech partners, encouraging better credit discipline. Over time, it is expected to improve asset quality and reduce stress in loan portfolios, particularly in unsecured and small-ticket lending segments.

Consumer Protection and Transparency

Borrower protection is a core pillar of the new framework. Lenders are required to clearly disclose loan terms, interest rates, and the identity of the lending entities. Customers must know whether their loan is being funded by a bank, an NBFC, or a combination of both.

Enhanced transparency is expected to reduce confusion, mis-selling, and unfair practices. For fintech platforms, this means clearer communication and tighter controls over marketing and onboarding processes.

Operational and Technology Challenges

Implementing the new guidelines will require adjustments in technology systems, data-sharing protocols, and operational workflows. Fintech startups may need to modify platforms to ensure seamless integration with regulated lenders’ systems and compliance requirements.

For NBFCs and banks, upgrading monitoring, reporting, and audit mechanisms will be essential. While these changes may increase costs in the short term, they also lay the foundation for scalable and compliant growth.

Industry Response and Strategic Shifts

The broader industry response to the new guidelines has been cautiously optimistic. Many stakeholders view the changes as a necessary step toward long-term sustainability. Fintechs are reassessing business models, focusing on partnerships rather than balance sheet risk, while NBFCs are strengthening governance frameworks.

Strategic collaborations are expected to become more selective, with greater emphasis on alignment of values, risk appetite, and compliance culture.

What This Means for the Credit Market

In the near term, some slowdown in co-lending activity is possible as players adjust to the new rules. However, over the medium to long term, the framework is likely to support healthier growth. Clearer rules reduce uncertainty and create a more predictable environment for innovation.

For borrowers, the changes promise greater protection and transparency. For lenders and fintechs, they offer a clearer roadmap for collaboration within defined regulatory boundaries.

The Road Ahead

RBI’s new co-lending guidelines reflect the regulator’s intent to support innovation without compromising financial stability. For fintech startups and NBFC partners, the message is clear: growth must be built on strong governance, transparency, and accountability.

Explained simply, the new framework does not shut the door on fintech-led lending—it formalises it. Those players willing to adapt, invest in compliance, and focus on responsible innovation are likely to emerge stronger in India’s next phase of digital credit expansion.

Also read – https://outlooknews.in/how-to-secure-your-home-from-cyber-frauds-a-survival-guide-for-2026/

Add outlooknews.in as preferred source on google – click here

Last Updated on: Tuesday, January 27, 2026 10:22 am by Outlook News Team | Published by: Outlook News Team on Tuesday, January 27, 2026 10:22 am | News Categories: India